---blog Title---

Customer Retention Strategies for Banks: 8 Ways to Drive Loyalty and Lifetime Value

---desktop---

---mobile---

In 2025, digital-first banking isn’t a choice anymore, it’s the baseline.

Customers now expect seamless, personalized, and on-demand financial experiences across every touchpoint. Yet, despite rapid digital adoption, most banks are still struggling to keep up.

And here’s the wake-up call. According to Zendesk’s 2025 Financial Services Experience Report, 84% of customers use online banking, and 72% rely on mobile apps as their primary way to interact with their bank. Yet 64% still report dissatisfaction due to clunky interfaces and unhelpful support.

This growing experience gap has paved the way for fintech challengers — agile, user-centric, and relentlessly innovative. They’re not just digitizing banking; they’re redefining what customers expect from it.

For traditional banks, the competition is no longer just other banks — it’s every frictionless, personalized digital experience customers encounter. To retain loyalty, banks must move beyond products and pricing and focus on building smarter, simpler, and deeply connected customer journeys.

In this blog, we explore what drives customer retention in banking today and share proven strategies leading banks use to build loyalty and stay ahead in an increasingly competitive landscape.

What is Customer Retention in Banking?

Customer retention in banking refers to the ability to maintain long-term relationships with customers, ensuring they continue engaging with the bank’s products and services instead of switching to competitors. Unlike customer acquisition, which focuses on attracting new clients, retention is about nurturing existing relationships, building trust, and enhancing loyalty.

Retention is more critical than ever in 2025. Loyal customers deliver a higher lifetime value by utilizing a broader range of financial products — savings accounts, credit cards, loans, investment plans, and even lifestyle add-ons like insurance or tax tools. Moreover, acquiring a new customer remains 5x to 7x more expensive than retaining an existing one.

Satisfied customers are not only more likely to stay, but they’re also more inclined to recommend the bank to friends and family, driving organic growth.

With generational shifts shaping expectations, modern bank retention strategies focus on:

- Lifestyle alignment

- Digital ease

- Proactive, personalized engagement

Gone are the days when outdated loyalty point models alone could keep customers.

However, friction at any touchpoint such as long wait times, complex procedures, poor customer service, or hidden fees can quickly lead to dissatisfaction and drive customers toward competitors.

Therefore, customer retention is a continuous process that requires banks to invest in customer experience, personalization, and digital transformation. By prioritizing retention, banks can increase customer lifetime value and build a stronger reputation in today’s highly competitive financial market.

---outlined-cta---

Comprehensive Approach to Affluent Client Acquisition - Download Now

Why Attracting and Retaining Bank Customers Matters More Than Ever

In 2025, customer retention in banking has become a strategic imperative, not just a support function. As the financial industry undergoes rapid transformation, the rise of digital banking, increased competition from fintech startups, and shifting customer expectations have made it crucial for banks to focus on both acquiring new customers and keeping existing ones engaged. Unlike in the past, when customers remained loyal to a bank for decades, today’s consumers have more choices than ever.

The ability to blend human empathy with digital speed is the holy grail of customer retention strategies in the banking industry. With mobile banking, AI-driven financial solutions, and digital wallets becoming mainstream, customers now expect convenience, speed, and security.

Another reason customer retention strategies for banks are more important than ever is the evolving nature of banking itself. Digital-first banks and fintech disruptors are redefining financial services with seamless mobile experiences, AI-powered financial tools, and lower fees.

Key Challenges Banks Face in Retaining Banking Customers

Banks are often flooded with emails detailing rival banks’ offers—zero fees, higher interest rates, and even fancy rewards programs. Their customers are hearing the same siren call. Banks need to resolve these retention challenges to prevent customer attrition.

Changing Expectations

Customers no longer look for just a safe place to keep their money. They want more—they want convenience, personalized services, and easy digital experiences. They expect their banking to be as simple as using their favorite apps. But when banks don’t meet these changing needs, two things happen:

- Some customers quietly share their frustration while waiting in long queues or struggling with clunky apps.

- Others simply leave, choosing banks that make things easier for them.

The Loss of Personal Connection

There was a time when visiting a bank felt personal—staff greeted customers by name and knew their needs. But with everything moving online, this human touch is fading. Customers often feel like just a number, which makes it harder for them to stay loyal. Banks need to find ways to bring back that warmth and personal connection, even in a digital world.

The Threat of Security Breaches

Data breaches are a big concern in banking. Even if a bank’s systems are secure, customers still worry about their personal information. Trust takes a hit, and banks find it hard to convince customers that their money and data are safe. With deep fakes and AI-driven fraud on the rise, banks must double down on trust, transparency, and visible safeguards to reassure digital customers.

The Complexity of Services

Banks often offer too many services, and it can feel overwhelming for customers. Simple tasks like applying for a loan or managing an account turn into a confusing process. What customers really want is clear, easy-to-understand options that work without hassle. Simple apps, accessible services, and flexible options for managing loans or investments keep customers satisfied.

Fierce Competition

Digital-first banks are entering the market, offering faster services, lower fees, and customized options like customer loyalty programs, etc. These modern solutions attract customers quickly. Traditional banks try to adapt, but old systems slow them down. The race to stay relevant in such a crowded market is tough.

The Weight of Fees

Customers are paying more maintenance charges, ATM fees, late penalties it all adds up. These costs frustrate people, especially when they feel they’re not getting enough value in return. Many start questioning if it’s worth staying.

8 Effective Strategies to Improve Customer Retention in Banks

These strategies aim to directly boost customer retention in banking by aligning with modern customer expectations.

1. Understand and even anticipate customer needs

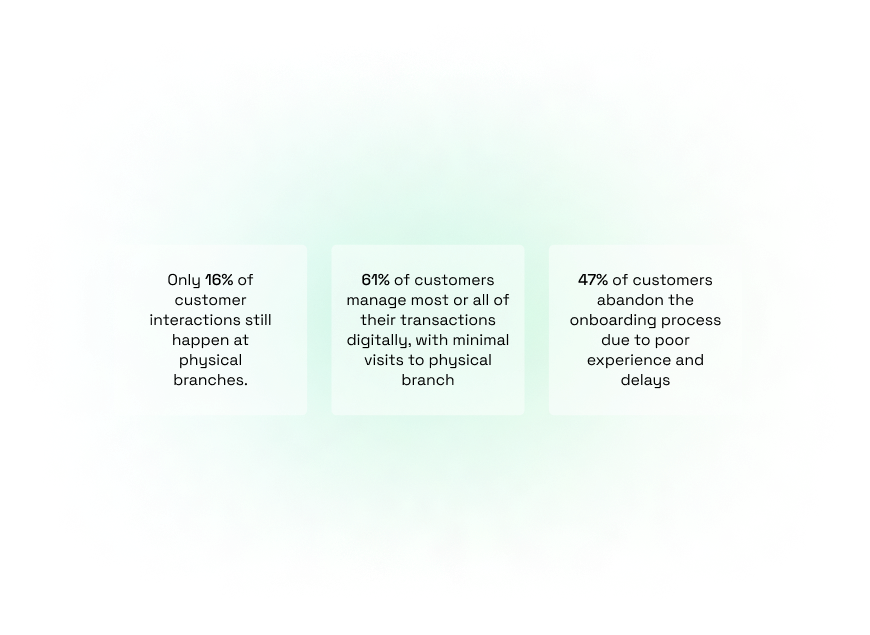

Customers no longer rely only on physical branches for their banking needs.

(Data source: World Retail Banking Report 2025, Capgemini)

While it is true that the needs of banking customers change depending on their age or affluence, (and it is vital for banks to know these needs), there are some needs that are universal and basic like security or fraud protection, and convenient mobile and online banking services.

This is on a very basic macro level.

Banks need to also be aware of milestone and event-based needs that could pop up for various customers and step in to address those needs. It is no surprise that customers today have very high expectations when it comes to banking services. And that is simply because they are used to the intuitive engagement, speed, and convenience offered by other brands, so much so that it has become a way of life for them and they want that from any brand they engage with. AI-powered segmentation now allows banks to anticipate financial milestones (like marriage, home-buying, or education loans) and proactively tailor offers before the customer even asks.

Tips about your customers to get you going

- Customers want things to be easy so offer them a simple, clean, seamless experience when they navigate your website or mobile app.

- Customers want multiple ways to connect with you they don’t want only a brick-and-mortar store. They want a website, they want a mobile app. And they want round-the-clock access to their information.

2. Offer the Customer what they see as Value

Same product but just more value!

Banks in general offer nearly identical products for nearly the same price. But to gain a competitive advantage they need to extend their product quality beyond core services to include additional features and value. For example, some banks offer remote deposits in the US where a person can scan the digital image of a check and transmit that to a bank without having to present the physical check at a branch.

In 2025, customers pay for value, not just features and strategies for customer retention must reflect this mindset shift. For example, if customers value convenience, they need to be offered services such as electronic banking, touch-tone phone account access, and internet banking.

To be more specific, if a 20-year-old customer logs into his bank account on his mobile phone:

- The bank can offer him a deal where he gets two free movie tickets per month if he spends a certain amount on his credit card every month. This will be more attractive to him than offering him a life insurance policy or wills and estate planning services.

- They can just let the customer pick and choose what he or she wants and, based on those choices, offer incentives, discounts or rewards.

Tips about your customers and what they value

- Customers want good deals, they will even exchange their private information for really good discounts or deals. So offer them things they value.

- Be different but don’t try to copy what another bank does. Customers want you to stand out from the others. So even if you offer a similar product, highlight the one thing that makes it different.

- Create a customer-centric culture in your bank that will translate into tremendous value to your clients.

3. Offer Hyper-Personalized engagement

The days of customers being happy with a simple personalized touch in emails or any communication from the bank are long gone. The evolved customer is accustomed to a lot more in today’s hyper-personalized scenario. And with the massive amounts of customer data that banks possess, it is very easy to hyper-personalize banks’ interactions with their customers.

---outlined-cta---

Strategic Insights for Acquiring High-Value Banking Clients - Download Now

Hyper personalization in banking is no longer optional it’s a necessity for effective customer retention in banking in a digitally saturated market. It starts by getting to know and understand each customer’s unique circumstances and preferences and then getting the right products and services served to them, accordingly.

For example, we helped a Malaysian banking client offer personalized loans to their customers based on their payment patterns. We used Adobe Analytics to capture their behavioral data and develop actionable insights to target each and every customer. This led to generating a large number of conversions.

By using data and analytics and assigning a dedicated relationship manager who knows and understands each customer’s unique and specific needs, banks can offer hyper-personalized services to their customers which can go a long way in preventing churn and increasing satisfaction and loyalty.

This is where customer retention strategies in the banking industry truly gain traction, using data to deliver one-to-one value at scale.

Tips to hyper-personalize your engagement with your customers

- Offer a bundle of services along with your product, for example, something like your credit card comes with roadside assistance and discounts at gas stations. The key is to offer customers bundled services in the area of their interest.

- Invest in a good MarTech stack to augment the one you already have, or to stand alone and handle customer data. That is crucial to hyper-personalization.

4. Increase Customer Satisfaction

What Makes Great Customer Service? Great customer service is about offering the right product and services to the right customers. It is also about finding issues that a customer faces and fixing them instantly.

Tracking the right metrics can significantly boost customer retention for banks. Key metrics include:

| Customer Retention Metrics | What It Measures |

| Retention Rate | The percentage of customers retained over time. |

| Churn Rate | The percentage of customers who leave. |

| Net Promoter Score (NPS) | How likely customers are to recommend your services. |

| Customer Lifetime Value (CLV) | The total value a customer brings to the bank over their lifetime. |

| Cross-Selling Ratio | How well banks are selling additional products to existing customers. |

For instance, we keep our clients updated with retention metrics like Customer Satisfaction scores, so that they can take the necessary measures when there is a drop or a spike. We conduct CSAT (Customer Satisfaction) surveys to arrive at these insights. Not only do these surveys reveal how satisfied the customers are, but also throw light on the pain points in their customer journey.

The bottom line is to keep customers happy. Recent Zendesk insights suggest that nearly half of banking customers consider switching banks due to a single poor service experience — even if the product itself is strong.

This is why banks have started to consolidate all the information that they have about their customers from all the various touch points, create complete profiles on each of them, and make these profiles available to all customer service representatives at various touch points so they can have meaningful conversations with them each time they engage with the bank.

---outlined-cta---

Download the guide to improve customer targeting for premium banking products

Tips to increase customer satisfaction

- Make the account opening process simple and quick. Works like a charm!

- Invest in a good data management system – holds great potential to facilitate excellent customer engagement, which will keep them happy.

5. Build up a Positive Corporate Branding or Image

Today’s banking customers have choices before them. Factors such as developments in technology, globalization, and increased consumer mobility have totally revolutionized the way people bank. And in order to do this, it is imperative that banks have a comprehensive knowledge of customers’ values, attitudes, and needs.

They need to see how the customer perceives the services that the bank offers and the image that they have of the bank itself. In such a scenario, branding can be a key differentiator. And differentiators can be what makes a brand.

For instance, a multinational banking client had been targeting locally as well as globally. We realized that their brand creatives across channels from their website to social, paid, and third-party channels, failed to align with their brand image. Based on whether the targeting was local or global, we helped them revamp their brand creatives and communications so as to adhere to their brand guidelines as well as resonate with their target audience worldwide. The brand now has a vibrant digital presence with millions of followers.

Tips to build a great brand image for your bank

- Embrace social media and use it to your advantage.

- Communicate clearly to your customers that you are a strong bank with low risks. That will go far in strengthening your appeal.

6. Increase Customer Loyalty

Increasing loyalty is one of the most measurable outcomes of successful customer retention in banking initiatives. Banks sell different products and services to customers, which increases customer loyalty apart from increased revenues alone. The more products a customer holds, the less likely he is to sever the relationship. The cost of selling one more product to an existing customer is just a fifth of the cost of selling it to a new one.

---outlined-cta---

“Cross-selling to a banking customer can be as simple as selling a credit card to an existing checking account customer. Or it could be selling a mortgage to an existing credit card customer.”

Customer loyalty first increases profits by reducing the cost of trying to acquire new customers. Loyalty is not the same as just retention. Loyalty is when customers opt to remain when there are other choices available. Banks, therefore, need to understand why the customer opts to stay and build on that.

It is no secret that banks that have strong customer loyalty have in front of them, an open door to win more of their customers’ business. A study by Gallup found that the customers who are ‘fully engaged’ with a bank are way more likely to buy more products from the same bank than those customers that are just ‘satisfied’.

Banks need to find ways to keep their customers loyal to them.

For example, one of our Middle Eastern clients had a loyalty program where they allowed customers to earn points by spending on any of their cards. The points can be redeemed for cash, merchandise, travel miles, gift cards that can be used in various places, etc. We integrated this program with the lifecycle campaigns we had been conducting such that each brand-loyal customer would receive personalized communications as soon as they became eligible.

Tips to increase customer loyalty in banks

- Improve customer service – nothing increases loyalty like great customer service

- Reward your customers – points, gifts, freebies, discounts. They all work!

7. Offer consistent experience on- and offline

Today, customers can engage with banks through various channels. They can walk into a brick-and-mortar store and connect with the bank through a mobile phone, or through the internet. While there are multiple channels that a customer can use, it is imperative that they be able to pick up from a channel right where they left off on another, and the messaging and communication from the bank remains the same across all channels.

Customers must be able to enjoy all banking services and features from any channel they choose – whether from a website, mobile app, bank’s branch, a call center, or any other available channel.

This is possible through advanced analytics and the linking of all the customer data so that regardless of the channel, the experience and the messaging remain the same.

When we realized that the target segments of a US-based banking client preferred a combination of offline and online services, we helped them develop online self-service channels along with round-the-clock support for availing credit cards, personal loans, and opening accounts. This would help provide a seamless customer journey irrespective of whether they prefer online or offline channels. This measure doubled the applications and reduced application times.

Tips to create great Omnichannel banking

- Use one unified integrated platform to drive consistent customer journeys.

- Offer an Omni-channel framework that is easy for customers to use. Consistency is vital here.

8. Place Switching Barriers

Banks often use strategies that make it harder or more expensive for customers to switch to another bank. These strategies include:

- Search Costs: The time and effort needed to find a new bank.

- Transaction Costs: Fees and paperwork involved in switching.

- Learning Costs: Time spent learning how to use a new bank's systems.

- Loyal Customer Discounts: Benefits exclusive to long-term customers.

- Emotional Costs: Building trust with a new bank takes time.

These factors create a “switching cost,” which holds customers back from leaving their current bank.

With the market being saturated, most banks realize that chances for any organic growth in banking are not that great. Therefore, customer retention strategies in the banking industry are more important than ever to combat switching behavior and protect long-term revenue.

Technology is a great enabler in this: to collate data and derive the right metrics to understand customer issues and use all this to improve service which will work in enhancing customer loyalty. Banks can understand the behavior of their customers and meet all their unique needs with tailored products and services, improving customer retention as a result.

For example, when we recommended a banking client to invest in a MarTech stack that builds unique customer profiles to provide a holistic view of its customers, they were surprised at the instant results. The unique profiles enabled us to hypertarget and personalize our communications based on customer preferences which reflected in increases in both acquisition and retention rates.

Mobile banking is another excellent strategy for banks to retain their customers. In the US, customers can apply for credit cards, and transfer their balances instantly via their smartphones, with no need for paperwork.

Tips for great switching barriers

- Entice customers to set up automatic payments ,they will hesitate to move and have to set it up all over again

- Charge transfer fees. Charge high!

Happy customers are a huge asset, they are brand ambassadors who will contribute immensely to enhancing brand value, increasing sales, and corresponding profitability.

Future Trends in Banking Customer Retention for 2025

In 2025, customer retention has evolved from being just a reactive strategy to becoming a proactive growth engine for banks. With hyper-connected customers and AI-driven insights, banks are reshaping how they engage and retain customers. Here’s what’s shaping the future:

1. Predictive Retention Models

Banks are no longer waiting for churn to happen. With AI-powered behavioral analytics, they can now predict customer attrition up to 60 days in advance. This allows relationship managers to offer personalized solutions, exclusive benefits, or financial wellness nudges before the customer even considers switching.

2. Experience Over Products

Unlike earlier, where loyalty hinged on interest rates or rewards, 2025 customers value experience above all. From frictionless onboarding to instant problem resolution and contextual financial advice, banks are investing heavily in experience-first retention models.

3. Integrated Human + Digital Touchpoints

Customers now expect personalized conversations backed by intelligent automation. In 2025, leading banks are combining relationship managers with AI assistants to provide a 360° engagement experience where human empathy meets digital intelligence.

FAQ on Effective Customer Retention in Banking

1. What is the key to retaining banking customers?

The key to customer retention is providing an excellent customer experience that meets their needs and expectations. This includes personalized services, easy-to-use digital banking platforms, and prompt support. When customers feel valued and satisfied, they are more likely to stay with their bank.

2. What is meant by customer retention rates in banks?

Customer retention refers to a company's ability to keep its customers over time. In banking, this means ensuring that customers continue to use the bank's services instead of switching to competitors. A high bank customer retention rate indicates that customers are satisfied and loyal, which is essential for a bank's long-term success.

To calculate the customer retention rate, you can use the following formula:

---outlined-cta---

Customer Retention Rate (%) = [(Number of customers at the end of the period - Number of new customers acquired during the period) / Number of customers at the beginning of the period] × 100

For example, if a bank starts the year with 1,000 customers, acquires 200 new customers during the year, and ends the year with 1,050 customers, the retention rate would be:

---outlined-cta---

Customer Retention Rate (%) = [(1,050 - 200) / 1,000] × 100 = 85%

This means the bank retained 85% of its existing customers over the year.

3. How can banks improve customer retention?

Banks can take several steps to improve customer retention in banking, including:

- Personalize Services: Offer products and services tailored to individual needs.

- Enhance Digital Experience: Ensure online and mobile banking platforms are user-friendly and efficient.

- Provide Excellent Customer Support: Be responsive and helpful in addressing customer inquiries and issues.

- Reward Loyalty: Implement programs that recognize and reward long-term customers.

4. Why do customers leave their bank?

Customers may decide to switch banks for several reasons:

- Unresolved issues or unhelpful staff can drive customers away

- Clunky digital banking platforms or inconvenient services

- Not-so-clear services and lack of ease of access can frustrate a customer

- A lack of personalized attention or engagement

- Competitors offering better rates or services may attract customers away.

- High fees and hidden charges

5. What are the most effective customer retention strategies in the banking industry today?

In 2025, the most effective strategies include hyper-personalization, predictive analytics for churn prevention, tiered loyalty programs, and seamless omnichannel experiences. Banks that blend tech-driven insights with human-centered design are leading the way in customer loyalty.